04 Apr 2024 Fiscal federalism vs Centre – State relations in India

Source – The Hindu and PIB.

General Studies – Paper – 2

Why in the News ?

- Recently, the Supreme Court of India has ordered to refer to the Constitution Bench a case filed by the State Government of Kerala, in which the decision of the Central Government in India to cut the borrowing given to the State of Kerala was challenged.

- The Supreme Court of India has refused to pass any order on the interim order restoring the situation before the imposition of the borrowing limit by the Central Government but has referred it to a larger bench which will provide an opportunity to examine whether the Central To what extent can the government regulate state borrowing? This step taken by the Supreme Court of India in this matter is a welcome development.

- The Kerala government has claimed in this case that the central government’s borrowing limit restriction violates the fundamental nature and provisions of India’s fiscal federalism.

The root cause of the dispute between fiscal federalism in India versus the state of Kerala :

- The issue has been filed by Kerala in the Supreme Court of India and the Center has net borrowing limit(NBC) refers to the imposition of restrictions, thereby limiting the borrowing capacity of any state in India.

- Kerala challenged the legality of the NBC in the Supreme Court, arguing that it hampers the state’s ability to finance essential services and welfare schemes.

Meaning of fiscal federalism in India :

- \Origin of the word fiscal ‘Fisk’ It is derived from the word which means public treasury or government money.

- Therefore, fiscal policy is related to the revenue and expenditure policy of the government.

- Fiscal federalism in India refers to the distribution of resources between the Center and the states.

- The distribution of taxes between the Center and the States is clearly mentioned in the Indian Constitution 7th schedule in India.

- There are 3 lists in the Constitution of India where taxes are distributed between the Center and the States.

They are as follows –

- Union list

- State list

- Concurrent list

Main objectives of fiscal policy in India :

The following are the objectives of fiscal policy in India-

- High economic growth

- Price stability

- Reduction in inequality

The above objectives are accomplished in the following ways –

- Consumption control – In this way, the ratio of savings to income is increased.

- Increasing the rate of investment.

- Taxation, infrastructure development.

- Imposition of progressive taxes.

- Weaker sections were exempted from taxes.

- Imposing heavy taxes on luxury items.

- Discouraging unearned income.

Main components of fiscal policy in India :

India’s fiscal policy mainly has three components. Which are as follows –

- Government receipts

- Government spending

- Public debt

All receipts and all types of expenditure of the Government in India are deposited and issued or spent from the following funds.

- Consolidated Fund of India

- Contingency fund of India

- Public account of India

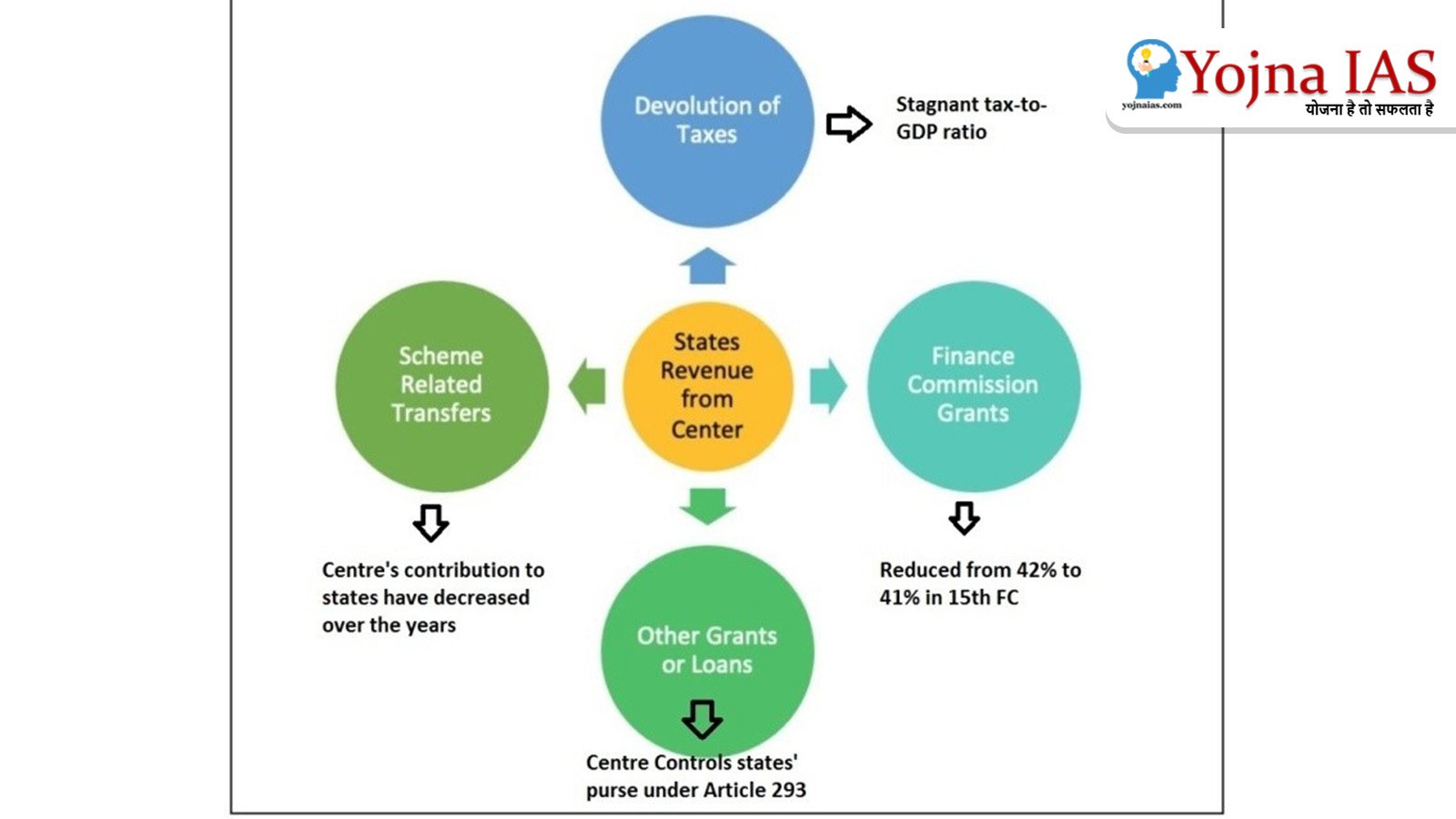

Net Borrowing Limit (NBC) :

- Net borrowing limit (NBC) is a restriction imposed by the central government on the borrowing capacity of states in India. In which it limits the amount of money under which any state in India can borrow either from the open market or from various sources.

- As of December 2023, the general net borrowing limit for states in India is ₹8,59,988 crore or 3% of state gross domestic product (GDP).

- However, the central government national pension scheme additional borrowing limit of ₹60,880 crore has been approved by 22 states of India to participate in NPS.

- The main objective of NBC is to regulate state finances, prevent excessive borrowing and ensure fiscal discipline in India.

Extra – Budgetary Borrowings covered under NBC :

- The Center has included loans taken by state-owned enterprises in the NBC. As such, statutory bodies in many states (such as the Kerala Infrastructure Investment Fund Board) cannot raise additional debt beyond the NBC’s 3% limit. The move has raised constitutional concerns regarding the right of the central government to regulate state finances.

Kerala’s argument in NBC’s case :

- Fiscal autonomy of states : The amendment made to the FRBM Act, 2003 violates the fiscal autonomy of the state by center.

- Borrowing limit : The Centre’s amendments have significantly reduced Kerala’s borrowing limit, impacting the state’s financial crisis management.

- Constitutional violation : Kerala argues that the Centre’s action is an encroachment on the state’s legislative domain, in violation of the provisions of the 7th Schedule of the Constitution.

- Financial Crisis : The state fears that without intervention, the financial constraints imposed could have long-term detrimental effects.

- Lump sum package : The move was suggested by the Supreme Court to help Kerala deal with the funding shortfall by imposing stringent conditions for the next financial year. The state rejected the loan of Rs 5000 crore because it would need about Rs 10,000 crore as loan.

Central Government’s argument :

- Financial crisis of the state : The Centre’s argument in this case is that Kerala’s financial crisis is due to the state’s mismanagement and wastage, and not due to borrowing limits.

- FRBM Act 2003 : Fiscal transactions between Center and states are governed by the FRBM Act, 2003, in which the borrowing limit is set at 3% of Gross State Domestic Product (GSDP).

- Recommendations of the 15th Finance Commission : The Center has refused to relax the borrowing limit citing the recommendations of the 15th Finance Commission. This led to Kerala exceeding the fiscal deficit target and high expenditure on salaries. “Highly indebted State” Is shown as. The Center said its one-time package offer (Rs 5,000 crore) comes with strict conditions to prevent other states from approaching courts for similar packages.

Fiscal Responsibility and Budget Management Act (FRBMA), 2003 :

- The main objective of the FRBM Act in India is to impose fiscal discipline on the government. Therefore, under this Act the government should conduct its fiscal policy in a disciplined manner or in a responsible manner i.e. the government deficit or borrowing should be kept within reasonable limits and the government should plan its expenditure according to its revenue so that the borrowing Stay within limits.

How is state borrowing regulated in India ?

- Article 293 : It provides financial autonomy to the states, allowing them to borrow only from within the territory of India on guarantee from the Consolidated Fund of the State.

- FRBM Act 2003 : The Fiscal Responsibility and Budget Management Act 2003 was enacted to ensure intergenerational equity in fiscal management. It states fiscal deficit and borrowing limits for both the central and state governments.

- Finance Commission : Finance Commission in India makes recommendations from time to time with respect to fiscal matters, including borrowing limits for the States, it is important to determine the borrowing limits for the States taking into account factors such as economic conditions, fiscal health and developmental needs .

- State Fiscal Responsibility Act : Each state may have its own fiscal responsibility act, which defines limits and guidelines for borrowing and fiscal management within the state.

- Role of the Centre : It plays an important role in overseeing financial matters, including approving borrowing limits for states based on the recommendations of bodies such as the Finance Commission. It can influence the state’s borrowing limits through legislative changes, amendments to existing laws such as the FRBM Act, or by exercising discretion in granting additional funds or by relaxing borrowing constraints in exceptional circumstances.

- Pay off debts : The state’s borrowings are used to finance ongoing expenses rather than profitable investments, affecting its credit rating.

- Revenue Generation : The state’s revenue generation may not be sufficient to meet its expenditure requirements, the state depends heavily on revenues from taxes including GST but fluctuations in economic activity and external factors affect tax collections.

- Expenditure System : There is a high level of recurrent expenditure on items like salaries, pensions and subsidies which creates financial imbalance in the state.

- Natural Disasters : Kerala is prone to natural disasters such as floods, landslides, etc., which can cause extensive damage to infrastructure and disrupt economic activities.

Solution / Way forward :

- Kerala’s challenge highlights an important constitutional dispute over fiscal federalism and state autonomy in financial management. The state argues that the Centre’s restrictions on borrowing, including loans of state-owned enterprises and public account balances, violate its constitutional rights. This legal battle highlights the tension between central oversight and state financial independence, potentially reshaping the dynamics of federal-state financial relations in India.

- Recommendations of the 15th Finance Commission To review again : Issues arising from the recommendations of the 15th Finance Commission may be re-examined. States can share their concerns with the Finance Commission or the Union Finance Ministry, so that states do not have to violate their fiscal autonomy while maintaining their fiscal stability.

- Need for judicial review and judicial clarification : Kerala has taken refuge in the Supreme Court of India in the NBC case. Hence, one solution is judicial review of the constitutional validity of NBC in relation to Article 293(3) and Article 266(2). The Court’s interpretation may resolve disputes related to the constitutional limits of the Centre’s authority over state borrowing.

- To cooperative federalism Need to strengthen : Regular high-level meetings between the Center and states through forums such as the GST Council or a specially convened Fiscal Policy Council can help facilitate interactions. The objective of these meetings will be to negotiate borrowing limits and ensure that states have sufficient financial leeway to meet their obligations.

- Legislative action : Parliament may consider making laws or amending existing laws (subject to constitutional limits) to clarify the scope of central monitoring over state borrowings. It should respect the balance of fiscal federalism and be prepared after extensive consultation with the states.

- Promoting fiscal responsibility at the state level : State fiscal management Can take proactive steps to strengthen, as Kerala has done through the Kerala Fiscal Responsibility Act. By setting clear deficit targets and budget management practices, states can demonstrate their commitment to fiscal prudence, potentially increasing their negotiating power with the Centre.

- Public account management Building consensus on : The issue of inclusion of public account withdrawals within the NBC can be addressed by creating a broad consensus among all the states, which can then be presented to the Center on a united front to exclude such transactions from the borrowing limit. ,

- By promoting economic reform and development : Economic reforms Expanding the tax base through taxation, promoting investment climate and promoting growth in the state’s own source revenue can be sustainable ways of ensuring adequate funding for state expenditure without dependence on borrowing.

Practice Questions for Preliminary Exam :

Q.1. Consider the following statements regarding fiscal federalism in India.

- The 7th Schedule of the Constitution deals with the distribution of taxes between the Center and the States.

- The restriction imposed by the central government on the borrowing capacity of states is called net borrowing limit (NBC) In India.

- Loans taken by state-owned enterprises are included in the NBC by the Centre.

- Setting borrowing limit restrictions for the states by the Center violates the fundamental nature and provisions of India’s fiscal federalism.

Which of the above statement / statements is/are correct?

A. Only 1, 2 and 3.

B. Only 2, 3 and 4.

C. Only 1, 3 and 4.

D. All of these.

Answer – D

Practice Questions for Main Exam :

Q.1. In recent years the concept of cooperative federalism has been increasingly emphasized. Throwing light on the shortcomings prevailing in the existing structure of cooperative federalism, discuss to what extent fiscal federalism will solve these shortcomings ? (UPSC CSE 2015)

Q.2 To what extent do you think cooperation, competition and conflict have shaped the nature of the union in India? Cite some recent examples to support your answer. (UPSC CSE – 2020)

Qualified Preliminary and Main Examination ( Written ) and Shortlisted for Personality Test (INTERVIEW) three times Of UPSC CIVIL SERVICES EXAMINATION in the year of 2017, 2018 and 2020. Shortlisted for Personality Test (INTERVIEW) of 64th and 67th BPSC CIVIL SERVICES EXAMINATION.

M. A M. Phil and Ph. D From (SLL & CS) JAWAHARLAL NEHRU UNIVERSITY, NEW DELHI.

No Comments