02 Feb 2024 Paytm Payments Bank Ltd forbidden from receiving new deposits

This article covers ‘Daily Current Affairs’ and the topic details of “Paytm Payments Bank Ltd forbidden by the RBI from receiving new deposits” .This topic is relevant in the “Indian Economy” section of the UPSC CSE exam.

Why in the News?

Paytm Payments Bank Ltd has been forbidden by the Reserve Bank of India from receiving new deposits and conducting credit transactions commencing in March 2024. This ruling essentially prevents Paytm Payments Bank from providing all of its main services, including accounts and wallets.

What does the RBI direction say?

- Prevented Paytm Payments Bank from providing almost all of its core services. After February 29, Paytm will no longer accept deposits or top-ups in any customer account, prepaid instrument, wallet, FASTags, National Common Mobility Card (NCMC), or other similar services.

- The RBI stated that the nodal accounts of parent company One97 Communications and Paytm Payments Services should be cancelled as soon as possible, but no later than February 29.

- Settlement of all pipeline transactions and nodal accounts, commenced on or before February 29, must be completed by March 15, and no transactions will be permitted beyond that date.

- Customers are free to withdraw or spend money from their Paytm accounts, which include savings and current accounts, prepaid instruments, FASTags, NCMC, and so on, as long as they do not exceed their available balance.

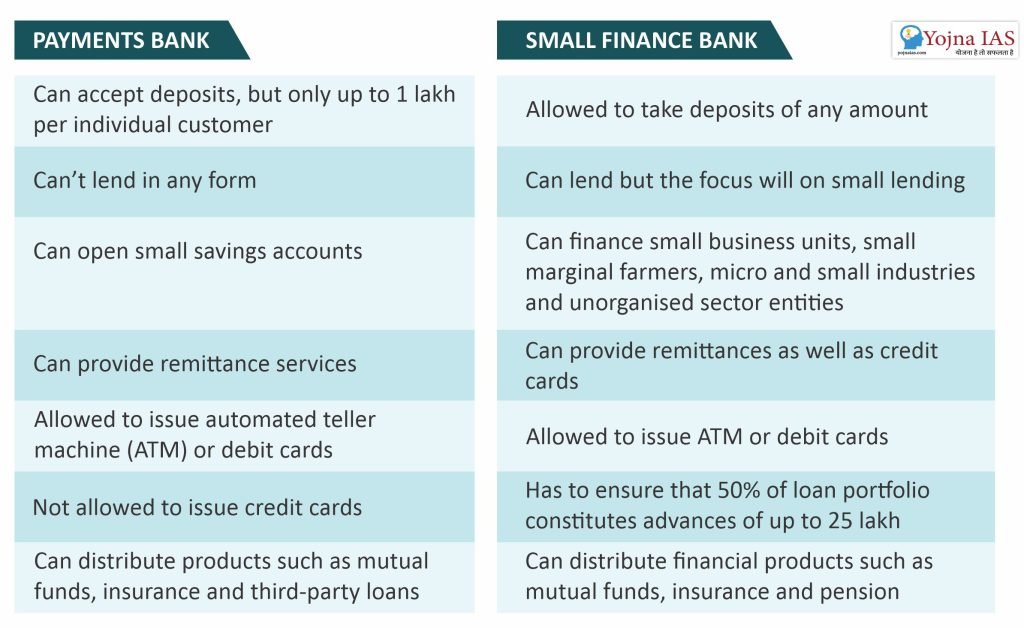

About payment banks?

- Payment banks, a brainchild of the Reserve Bank of India (RBI), emerged in 2014 as a new breed of financial institutions aimed at bridging the gap between traditional banks and unbanked segments of the population. It was based on the recommendations of the Nachiket Mor Committee. Unlike their full-fledged counterparts, payment banks come with a distinct set of features and limitations, catering to a specific financial needs

Key Characteristics of Payment Banks:

- Limited deposit taking: Payment banks can accept deposits up to ₹200,000 per customer, encouraging convenient savings without hefty initial sums.

- No credit facilities: Unlike traditional banks, they cannot issue loans or credit cards, focusing solely on deposit and payment services.

- Digital-first approach: They leverage technology to provide digital and mobile banking solutions, ensuring wider accessibility and financial inclusion.

- Basic financial products: They offer services like bill payments, money transfers, debit cards, and limited overdraft facilities.

Benefits for Customers:

- Easy access to banking: Payment banks simplify entry into the formal financial system, especially for individuals who lack access to traditional bank branches.

- Convenient digital services: Their digital focus makes banking more accessible and user-friendly, particularly for tech-savvy customers.

- Security and regulation: Backed by the RBI, payment banks offer a secure environment for deposits and transactions.

- Financial inclusion: They play a crucial role in bringing unbanked and underbanked populations into the mainstream financial system.

- Low-Cost Services: Payment banks often operate with lower overhead costs due to their digital-first approach and limited service offerings.Thus, can provide services with lower fees and reduced or no minimum balance requirements.

- Quick and Easy Account Opening: Payment banks often simplify the account opening process, allowing users to register and access basic banking services quickly.

Limitations to Consider:

- Deposit restrictions: The cap on deposits might not suit individuals with higher savings requirements.

- Limited product range: The absence of credit facilities and certain investment options restricts their service scope compared to traditional banks.

- Transaction charges: Some payment banks levy transaction charges, which might not be ideal for frequent users.

- Dependency on Technology Infrastructure: Payment banks heavily rely on technology for their operations. Any disruptions in digital services can hinder their ability to provide services.

- Low Transaction Volumes: In certain regions or during economic downturns, payment banks may face challenges in achieving sufficient transaction volumes.

India right now has 6 Payment Banks:

- Airtel Payment Bank

- India Post Payment Bank

- Fino payment bank

- Paytm Payment Bank

- NSDL Payment Bank

- Jio Payment Bank

Download Yojna daily current affairs eng med 2nd feb 2024

Prelims practice questions

Q1) Consider the following statements:

1) 200,000 is the maximum deposit amount allowed in a payment bank.

2) Payment banks can provide loans to farmers

3) Payment banks primarily operate through online platforms

How many of the above statements are correct?

a) One

b) Two

c) Three

d) None

ANSWER: B

Q2) What is the name of the government initiative that aimed to boost financial inclusion through various measures, including the introduction of payment banks?

a) Pradhan Mantri Jan Dhan Yojana (PMJDY)

b) Atal Pension Yojana (APY)

c) Stand Up India

d) Beti Bachao Beti Padhao

ANSWER: A

Mains practice question

Q1) Evaluate the effectiveness of financial literacy initiatives conducted by payment banks in educating users about the benefits and responsible use of digital banking services.

I am a content developer and have done my Post Graduation in Political Science. I have given 2 UPSC mains, 1 IB ACIO interview and have cleared UGC NET JRF too.

No Comments