15 Mar 2023 SILICON VALLEY BANK (SVB) CRISIS

SILICON VALLEY BANK (SVB) CRISIS

This article covers “Daily Current Affairs” and the topic details the recent Silicon Valley Bank crisis (SVB) crisis. The collapse of SVB, a US-based bank forced depositors to withdraw their money fearing the chances of it turning insolvent.

For Prelims:

- Basel Norms: The international banking regulations.

- Basel Committee on Banking Supervision (BCBS).

- Basel Accords and Indian Banks’ adherence to them.

For Mains:

- GS 3: Economy – Bond price and change in interest rates.

Why in the news?

The collapse of Silicon Valley Bank (SVB) has stoked fears about the vulnerability of the US banking structure. It also signifies the inherent weaknesses of the banking sector. The crisis can have spillover effects on the financial sector on a global level.

Silicon Valley Bank

What is Silicon Valley Bank (SVB)?

SVB is a US-based bank established in 1983. Before the collapse, it was the 16th largest US-based bank, which provided services to over fifty percent of venture-backed technology companies in the US.

The Silicon Valley Bank is known for its close relationships with the technology and innovation industries, and it has helped finance some of the most prominent technology companies in the world. It has also been involved in several notable IPOs and mergers and acquisitions in the technology sector.

Silicon Valley Bank provides a range of banking and financial services, including loans, credit cards, foreign exchange, cash management, and investment services.

What went wrong and caused the Crisis?

The Silicon Valley Bank was shut down by US regulators. The liquidity situation was dismal as the bank fell short of cash to pay its depositors.

The wrong investment decisions made by Silicon Valley Bank are considered the primary reason behind the crisis. The Bank invested a major portion of its wealth in government bonds when the interest rates were low.

Government bonds are considered the safest option with near to zero chances of default. But the problem started with the hike of interest rates by the US Fed to counter the inflationary pressure developed as a result of the pandemic and geopolitical conflicts. As a result, the bond prices of Silicon Valley Bank took a plunge leading to major losses.

Impact of changes in the interest rate on Bond yields

Bond yields and prices have an inverse relationship, meaning that as bond prices increase, bond yields decrease and vice versa. This is because the yield of a bond is calculated as the coupon rate (the fixed interest rate paid on the bond) divided by its price. (Bond Yield = Coupon Rate / Bond price)

Any kind of change in the interest rates impacts bond prices.

- Decrease in interest rate: The price of existing bonds will increase, as their fixed coupon rate becomes more attractive relative to the lower prevailing interest rates. This will cause the bond’s yield to fall.

- Increase in interest rate: The price of existing bonds will decrease, as their fixed coupon rate becomes less attractive relative to the higher prevailing interest rates. This will cause the bond’s yield to rise.

What is the plan of action to deal with the Silicon Valley Bank Crisis?

- Federal Deposit Insurance Corporation or FDIC has taken over the wealth of Silicon Valley Bank.

- Federal Reserve has announced a thorough inquiry into the Bank.

- The US government has announced a tighter regulatory framework and a bailout package to tide over the crisis.

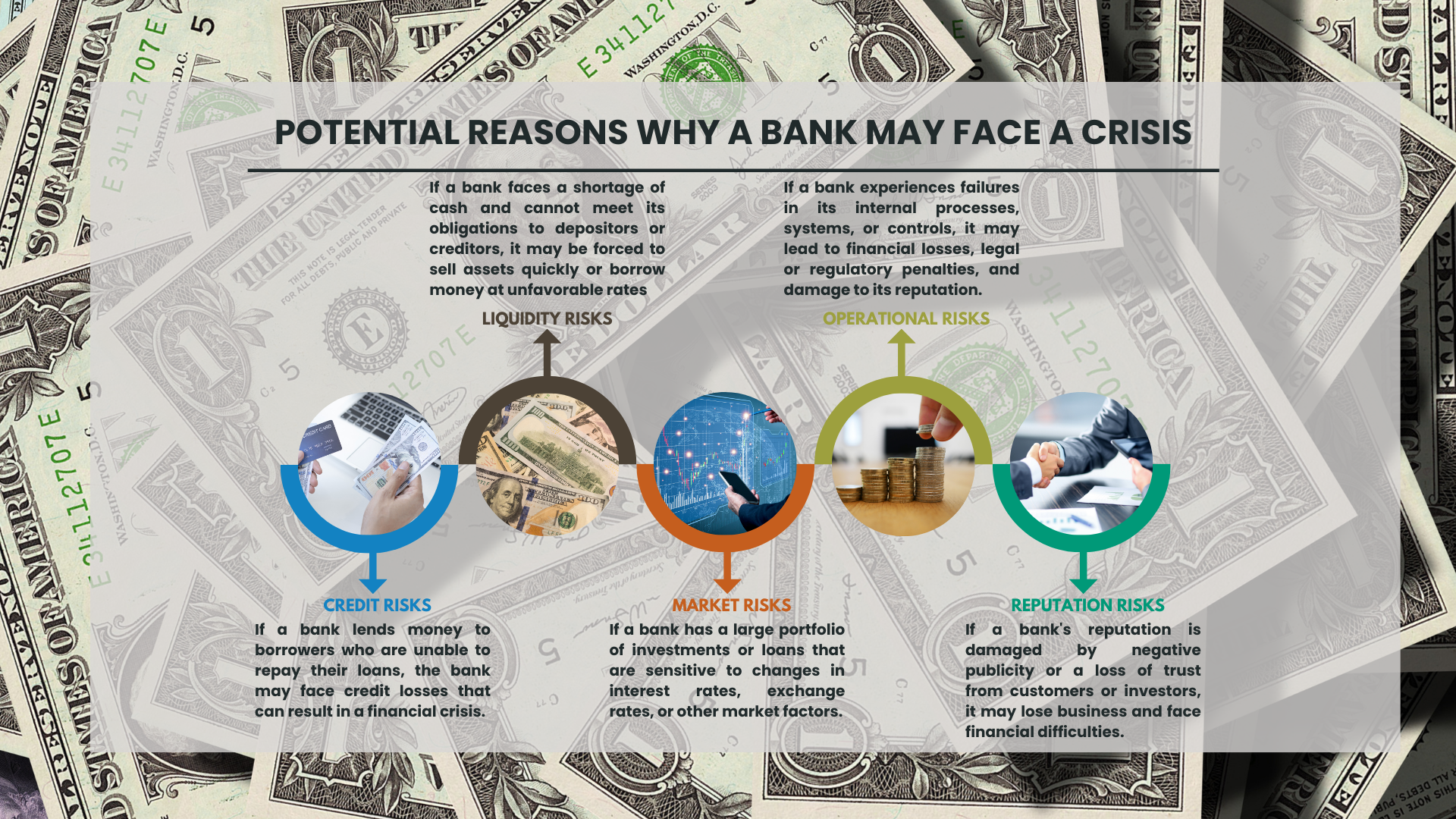

What are the situations when a bank faces collapse?

- Credit risks: If a bank lends money to borrowers who are unable to repay their loans, the bank may face credit losses that can result in a financial crisis.

- Liquidity risks: If a bank faces a shortage of cash and cannot meet its obligations to depositors or creditors, it may be forced to sell assets quickly or borrow money at unfavorable rates, which can lead to a liquidity crisis.

- Market risks: If a bank has a large portfolio of investments or loans that are sensitive to changes in interest rates, exchange rates, or other market factors, it may be exposed to market risk that can result in significant losses.

- Operational risks: If a bank experiences failures in its internal processes, systems, or controls, it may face operational risks that can lead to financial losses, legal or regulatory penalties, and damage to its reputation.

- Reputation risk: If a bank’s reputation is damaged by negative publicity or a loss of trust from customers or investors, it may lose business and face financial difficulties.

Way Forward

The collapse of the Silicon Valley Bank has sent a ripple effect around the world with stock prices taking a plunge. There are fears of financial uncertainties and risk of liquidity in the coming times. Some experts are marking the crisis as the largest bank crisis after the 2008 economic meltdown carrying the potential of spreading to other sectors while others are seeing it just as a transient phenomenon.

YOJNA IAS DAILY CURRENT AFFAIRS ENG MED 15th MARCH

Source:

Get current affairs from Yojna IAS

No Comments