03 Apr 2024 Gross Goods and Services Tax (GST) collections in India March 2024

Source – The Hindu and PIB.

General Studies – Development of Indian Economy, Gross Goods and Services Tax, Union Finance Ministry, Devolution of Central Taxes under Centre – State Relations in India

Why in the News ?

- This is the first time in the historical journey of revenue and total tax collection in India that for the first time in a financial year, the total collection of Gross Goods and Services Tax (GST) has crossed Rs 20 lakh crore.

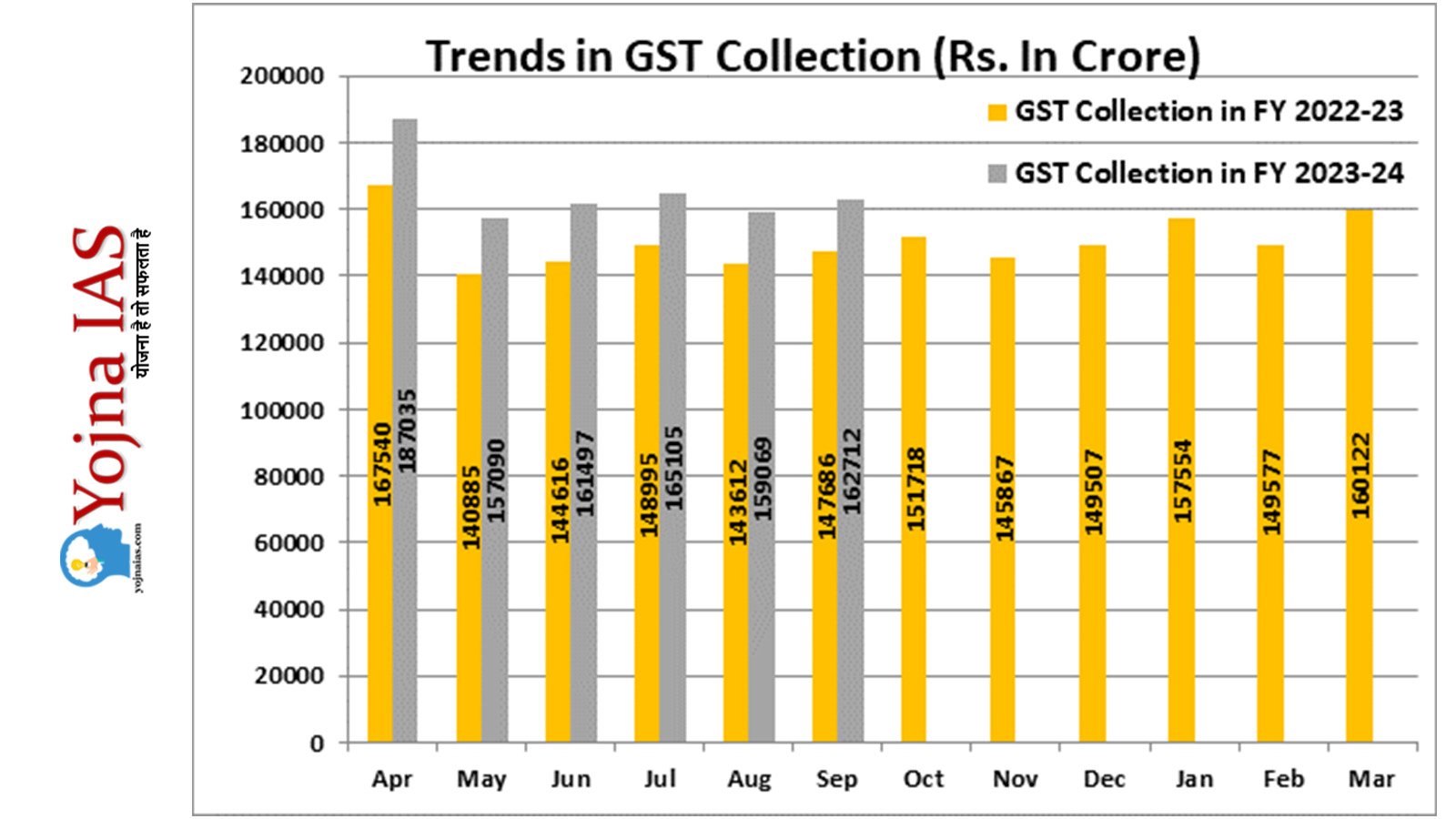

- The total gross GST collection in the financial year 2023-24 was Rs 20.18 lakh crore, showing a growth rate of 11.7% over the previous financial year.

- The average monthly collection for fiscal year 2023-24 was Rs 1.68 lakh crore, higher than last year’s average tax collection of Rs 1.5 lakh crore.

- The net GST revenue after settlement till March 2024 for the current financial year is Rs 18.01 lakh crore, showing a growth rate of 13.4 per cent compared to the same period last year.

- The highest gross GST collection in India in March 2024 was Rs 1.78 lakh, which is an increase of 11.5% over the previous year i.e. March 2023.

- This was the second highest monthly collection of GST in a month since the implementation of GST in India in the month of July 2017.

- The highest ever single-month gross GST collection of Rs 1.87 lakh crore was achieved in India in the month of April 2023.

- According to the Union Finance Ministry, the main reason for the highest gross GST collection in March 2024 is the increase in domestic transactions.

- Net GST revenue after refund in March 2024 in India is Rs 1.65 lakh crore, which is 18.4% higher tax collection compared to the same period last year.

- Maharashtra ranks first in GST collection in India in March 2024. In India, only the state of Maharashtra has the highest contribution to the total tax collection of Rs 27,688 crore.

India has witnessed a positive performance across all components of tax collection. Therefore, the details of total tax collection in March 2024 are as follows –

- Central Goods and Services Tax (CGST): ₹34,532 crore

- State Goods and Services Tax (SGST): ₹43,746 crore

- Integrated Goods and Services Tax (IGST): ₹87,947 crore, including ₹40,322 crore collected on imported goods.

- ₹12,259 crore in cess, which includes ₹996 crore collected on imported goods.

Details of gross GST collection in the financial year 2023 – 24 :

The contribution of various sectors in GST collection during the financial year 2023 – 24 is as follows –

- Central Goods and Services Tax (CGST) Rs 3,75,710 crore,

- State Goods and Services Tax (SGST) Rs 4,71,195 crore;

- Integrated Goods and Services Tax (IGST) was Rs 10,26,790 crore, which also includes Rs 4,83,086 crore collected on imported goods.

- Cess: Rs 1,44,554 crore collected, including Rs 11,915 crore on imported goods.

Some important facts related to Goods and Services Tax in India :

- The continued strong performance in terms of total gross GST collections in India in FY 2023-24 is a milestone. The average monthly tax collection this financial year is ₹1.68 lakh crore, which is higher than last year’s average of ₹1.5 lakh crore.

- The GST revenue net of refunds till March 2024 for the current financial year is ₹18.01 lakh crore, an increase of 13.4% over the same period last year.

- Under the Inter-Governmental Settlement in India, in the month of March, 2024, the Central Government has settled ₹43,264 crore to CGST and ₹37,704 crore to SGST from the collected IGST.

- In India, this amounts to a total revenue of ₹77,796 crore for CGST and ₹81,450 crore for SGST for March, 2024 after regular settlement in terms of taxes.

- For FY 2023-24, the Central Government has settled ₹4,87,039 crore to CGST and ₹4,12,028 crore to SGST from the collected IGST.

What is Goods and Services Tax ?

- GST is known as Goods and Services Tax. It is an indirect tax which has replaced many indirect taxes in India like excise duty, VAT, service tax etc.

- Goods and Services Tax (GST) was passed by the Parliament in India on 29 March 2017 and this tax system was implemented across India from 1 July 2017.

- Goods and Services Tax was included in the Constitution of India by the 101st Constitutional Amendment Act 2016.

- This Amendment Act made provision for Goods and Services Tax by including a new Article 246A in the Constitution.

- Goods and Services Tax (GST) It is imposed on the supply of goods and services.

- The Goods and Services Tax law in India is a comprehensive, multi-stage, destination-based tax that is levied on every value addition.

- GST is a single domestic indirect tax law for the entire country.

- The Goods and Services Tax has simultaneously replaced almost all the indirect taxes imposed by the Central Government and the State Government.

Indirect taxes in India which have not been replaced by GST. Well the tax is as follows–

- Basic customs duty

- Value added tax on petrol and diesel

- Tax on tobacco and alcohol

- Stamp duty on property

- Electricity charges

- Vehicle tax

- Property tax

Process of transfer of central taxes under Centre-State relations in India :

- The central government transfers taxes to the states on the basis of the recommendations of the Finance Commission. Which is transferred through monthly installments.

- In the last two years, a significant portion of the total funds were transferred in the latter half of the financial year.

- In 2021-22, the Center transferred 50% of the funds during the fourth quarter (January-March). This figure was 36% in 2022-23.

- In the first quarter (April-June) of 2023-24, the Center has transferred 23% of the total funds allocated to the states.

- This is significantly higher than 2021-22 and 2022-23. Advance transfer of central taxes may allow states to avoid spending in the final months of the financial year.

- According to the General Financial Rules, 2017 issued by the Finance Ministry of India – excess of expenditure in the last months of the financial year is considered a violation of propriety.

- The uneven pace of expenditure by states in a financial year may be affected by the patterns of receipts. Tax transfers from central taxes to states may also allow states to better plan their expenditure patterns during that financial year.

Solution / Way forward :

- The journey of GST in India so far and the huge surge in GST revenues provide an opportunity to make some much needed reforms in this tax system, indicating the opening of a window for GST.

- The surge in overall GST growth should allow the next government to be formed after the Lok Sabha general elections in 2024 to focus on much-needed reforms in this tax system.

- The increase in GST collections is due to tax demands made for previous years and crackdown on known methods of tax evasion such as fake invoices and fraudulent input tax credits.

- Therefore, the government also needs to tighten its grip on tax evaders in India so that a transparent tax system can be ensured in India.

- These reforms should include reimagining the plan to rationalize this tax by removing different rates and bringing excluded items like electricity and petroleum products under its ambit and reducing high duties on key products like cement and insurance. .

- The GST compensation cess, which is now being used to compensate states for repaying COVID-19 pandemic-era borrowings, was worth Rs 1.44 lakh crore last year, before being settled before the extended deadline of March 2026. Let it be given.

- It is extremely important for the Central Government to avoid the temptation to impose implicit cess except on genuinely demerit items like tobacco.

- Imposing taxes on hybrid vehicles at more than 40 per cent, despite encouraging consumption and private investment, will make it difficult for India to achieve its green goals. Therefore, the Central Government also needs to rationalize this existing tax system, so that India can easily and successfully achieve its green target.

Download Yojna daily current affairs eng med 3rd April 2024

Practice Questions for Preliminary Exam :

Q.1. Consider the following statements regarding Goods and Services Tax (GST) in India.

- Goods and Services Tax in India has been implemented by the 101st Constitutional Amendment Act 2016.

- GST in India is a single domestic indirect tax law for the entire country.

- The contribution of Central Goods and Services Tax (CGST) is ₹34,532 crore while the contribution of State Goods and Services Tax (SGST) is ₹43,746 crore in India in March 2024.

- Taxes on tobacco and alcohol and property tax are also included in GST In India.

Which of the above statement / statements is/are correct ?

A. Only 1, 2 and 3.

B. Only 2, 3 and 4.

C. Only 3 and 4.

D. Only 1, 3 and 4.

Answer – A

Practice Questions for Main Exam :

Q.1. What do you understand about the Goods and Services Tax? Discuss in detail the effects of GST on the Indian economy, its challenges and its solutions.

Qualified Preliminary and Main Examination ( Written ) and Shortlisted for Personality Test (INTERVIEW) three times Of UPSC CIVIL SERVICES EXAMINATION in the year of 2017, 2018 and 2020. Shortlisted for Personality Test (INTERVIEW) of 64th and 67th BPSC CIVIL SERVICES EXAMINATION.

M. A M. Phil and Ph. D From (SLL & CS) JAWAHARLAL NEHRU UNIVERSITY, NEW DELHI.

No Comments